Dubai has slowly turned into a hub for fintech companies. In the first half of 2025 alone, over 1,081 new active registered companies joined the Dubai International Financial Centre (DIFC), with fintech and innovation companies rising to 1,388 from 1,081 the year before. That’s one of the fastest climbs anywhere in the world. While Silicon Valley debates crypto regulations and London grapples with the Brexit aftermath, Dubai is quietly shaping one of the world’s most entrepreneur-friendly fintech ecosystems.

The momentum is clear. Company registrations at DIFC surged 32% year-on-year, according to Reuters, showing how quickly startups are choosing Dubai as their launchpad. And with investor capital, regulatory clarity, and zero personal income tax, many fintech founders setting up a fintech company in Dubai are finding a faster path to profitability compared to global peers.

Why Setting up Your Fintech Company in Dubai?

Dubai and the wider UAE have emerged as leading fintech hubs by combining global regulatory standards with local strategic incentives. The country offers zero percent corporate tax for qualifying free zone companies, 100% foreign ownership without local partners, and an English common law framework that provides international comfort.

Add 48-hour visa processing for key personnel and direct access to 3.5 billion consumers across Africa, Asia, and the Middle East, and the appeal becomes clear for anyone starting a fintech company in Dubai.

The real game-changer isn’t just what Dubai offers but how it’s reimagined fintech regulation itself. Most countries treat fintech like traditional banking with slight modifications. Dubai built entirely new regulatory frameworks from the ground up. Below are the mentioned features that makes Dubai a global hub for FinTech companies:

Clear and progressive regulations

Dubai is unique in that it doesn’t leave fintech firms uncertain. Dubai Financial Services Authority (DFSA) and the Virtual Assets Regulatory Authority (VARA) have developed clear structures on digital payments, blockchain, and cryptocurrencies. The DIFC Innovation Hub also allows start-ups to test products under a regulatory sandbox before they come into existence. For fintech company in Dubai this structured environment reduces the risk of compliance, speeds up approvals and gives investors confidence.

Robust government support for fintech

The fintech ecosystem in the city has the support of a vision of policy over the long term. Programs like the Dubai Economic Agenda (D33), doubling the size of the economy over the course of the decade, and the Cashless Dubai initiative, with 90% of transactions to go digital by 2026, enhance digital finance uptake directly. The UAE Centennial 2071 plan also identifies fintech as one of the pillars for economic diversification in the future. For start-ups, this means access to government accelerators, policy support, and a market that’s being pushed toward digital finance every day.

Availability of substantial capital bases.

Funding in fintech is at unprecedented levels. The UAE fintech market was estimated at USD 3.16 billion in 2024 and estimated to reach USD 5.71 billion by 2029 at a CAGR of 12.56. In fintech, venture capital was also a leading source of funding in the UAE, with H1 2024 representing 32% of all funding. Although it is possible to raise money in a few days, start-ups have an even better opportunity to be seen by worldwide VCs and other private equity funds when they head to Dubai, known as the home of the majority of fintech firms and investors.

A hub connecting fast-growing markets

Dubai’s geographic advantage is unmatched. Placed at the intersection of the Middle East, Africa, and South Asia markets with a total population of more than 3 billion individuals, most of whom are unbanked, it provides fintechs entry points to high-demand markets. The MEASA fintech market in itself is anticipated to almost double by 2029. From e-wallets to remittance services, firms in Dubai are able to test in an innovative local market and then scale regionally without having to relocate base, making it a launchpad to some of the fastest-growing economies in the world.

Infrastructure and digitally enabled consumers

The UAE boasts more than 99% and one of the world’s highest rates of smartphone penetration. Customers are already used to digital banking and online payments, and the Dubai Cashless Economy initiative makes sure that uptake continues to rise. For fintech start-ups, that translates to quicker user acquisition, reduced education costs, and high demand from day one. Added to the advanced digital infrastructure from cloud services to secure data centers, the ecosystem enables businesses to scale rapidly without the bottlenecks typical in less digitally evolved markets.

Strict IP laws

When ideas are patented, innovation increases. Dubai has revised the laws on intellectual property to be in line with international standards, which affirms fintech company in dubai that their technologies, brands, and digital assets are secure. This security does not only give the investors confidence but also emboldens the entrepreneur to innovate and introduce even more ideas to the market since this is where innovation, in turn, drives growth and vice versa.

What makes UAE fintech regulations work?

The growth in the UAE’s fintech space has primarily been driven by initiatives from the UAE’s two financial free zones: the Dubai International Financial Centre (DIFC) and the Abu Dhabi Global Market (ADGM).

Both have established their own fintech hubs with the ADGM Regulation Lab (RegLab) and the DIFC Innovation Hub.

This creates a dual-track system. Companies can choose the fast lane with sandbox environments where they test ideas with minimal regulation or take the highway route with full licensing for proven concepts and clear pathways.

Recent updates for 2024-2025 include Open Finance Regulations that require banks to share data through APIs, Payment Token Services with clear rules for stablecoins and digital currencies, and Sandbox Extensions that allow testing periods up to 24 months.

The approach functions as “regulation as a service” where companies get exactly what they need, when they need it, rather than wrestling with outdated frameworks designed for traditional banking.

How Dubai Powered the Region’s First Fintech Unicorn

In 2019, a well-known company was established in Dubai, and in 2023, it became the first fintech unicorn of MENA, having raised a Series D of 200 million dollars, and being valued at 1.5 billion dollars. Their experience provides useful insights to anyone launching a fintech firm in Dubai.

The History: The company was founded in Dubai and was initially dealing with Buy Now, Pay Later (BNPL) services as it saw an opportunity in the regional market to fill a gap that offered flexible options in terms of payment.

Dubai as a strategic Growth: The company has used the Dubai regulatory environment to grow fast. They capitalized on the GCC region by taking advantage of business-friendly policies of the emirate to expand.

Key Success Factors:

- Started with clear regulatory compliance from day one.

- Results oriented towards addressing actual customer issues (flexible payments).

- Established relationships with more than 30,000 international brands, such as Amazon and SHEIN.

- Scaled rapidly – currently handling more than $6 billion of annual transaction volume with 10 million users.

The Expansion: This fintech company in 2023, moved its headquarters to Saudi Arabia, which showed how Dubai can be used as a launchpad to expansion in the region.

Lessons for New Entrepreneurs:

- Use Dubai’s regulatory sandbox to validate your concept.

- Focus on solving regional problems, not copying Western models.

- Build strong partnerships with established brands.

- Plan for regional expansion from day one.

- Prepare for eventual IPO – Tabby is planning to list on the Saudi stock exchange.

The company’s success shows the potential for fintech companies in Dubai. They went from startup to unicorn in just four years by leveraging Dubai’s advantages while staying focused on customer needs.

Where should you set up your fintech company in the UAE?

Your choice between Dubai’s fintech zones can make or break your fintech company in Dubai. This isn’t a one-size-fits-all decision, and understanding the differences is crucial.

Dubai International Financial Centre (DIFC)

DIFC serves as the established player, perfect for payment processors, wealth management platforms, and established companies seeking credibility. The zone offers the FinTech Hive accelerator program, extensive banking partnerships, and premium brand recognition. However, every DIFC firm must lease physical space within the district. Hot-desk style flex offices start around thirty-five thousand dollars annually for a two-person room, while mid-sized fitted offices generally cost between fifty-five and ninety dollars per square foot.

Abu Dhabi’s International Financial Centre (ADGM)

ADGM functions as the innovation hub, ideal for crypto and blockchain ventures, AI-powered financial services, and experimental business models. The zone provides highly flexible RegLab testing for up to 24 months, lower initial costs during testing phases, and faster application processing.

Mainland

Business setup in mainland will enable you to conduct business anywhere within the UAE without any limitations to free zones. The local market, government contracts, and collaboration with local banks are best with the mainland companies, which prefer direct access to the local market. The cost differs with the kind of license and activity and is usually between AED 50,000 -AED 200,000 without the office rent and compliance.

The approval processes may be more lengthy than free zones and the establishment of a bank may need more documentation, but the advantage is the availability to a larger customer base and government projects.

| Factor | DIFC | ADGM | Mainland |

|---|---|---|---|

| Setup Time | 3-4 months | 2-3 months | 4-6 months |

| Initial Investment | $75,000-150,000 | $50,000-100,000 | AED 50,000-200,000 |

| Sandbox Duration | 12 months | 24 months | Not typically available |

| Primary Strength | Banking integration | Regulatory flexibility | Market access and government contracts |

| Best for | Proven models | Innovation experiments | Local market presence and large-scale operations |

| Ownership | 100% foreign in free zone | 100% foreign in free zone | 51% local partner (some exceptions) |

What are the license types for your fintech company in Dubai?

Understanding license types is crucial. Choose wrong, and you’ll face delays and extra costs.

Innovation Testing Licence (ITL)

The ITL allows startups to test their fintech ideas in a controlled environment before moving into full operations. It provides flexibility while ensuring regulatory oversight. This licence is usually granted for 6 to 12 months and is most suitable for early-stage companies validating new concepts.

DIFC Innovation Licence

Designed to make entry into the Dubai International Financial Centre simple and affordable, this licence gives young companies access to the region’s leading fintech hub. With an annual fee of around USD 1,500 (subsidised for the first few years), it also opens doors to the DIFC FinTech Hive and networking opportunities. It is ideal for startups building credibility and seeking mentorship.

DFSA Category 3 & 4 Licences

These licences apply to firms that are ready to provide regulated financial services.

- Category 3 is required for activities such as payment processing and money transfers.

- Category 4 applies to businesses offering investment advice, portfolio management, or wealth services.

Capital requirements vary depending on the exact activities, ranging from several hundred thousand dirhams to a few million. These licences are best suited to fintech companies that are ready for full-scale operations.

Virtual Assets Licence (VARA or DFSA)

Organizations dealing with cryptocurrencies or other digital assets are required to acquire a licence of the virtual assets. In DIFC, this is covered by the DFSA, whereas in the non-DFC it is covered by the Virtual Assets Regulatory Authority (VARA). Activities that are included in the licence are exchanges, custody, transfers, and advisory services, and compliance and security are highly demanded. Crypto exchanges, blockchain platforms, and digital asset providers are the most applicable.

What are the steps to start a fintech company in Dubai?

Starting a fintech company in Dubai means following a clear process. Even a small error can set you back for months, so attention to detail is key.

Step 1. Choose the right jurisdiction

Your choice here shapes costs, market reach, and growth potential. Consider your customers, business model, and long-term vision.

- Mainland Company: Would be better in case you intend to go directly to the UAE market, or deal with government contracts, or deal with conventional banking.

- Free Zone Company: DIFC is highly credible and globally recognized, whereas ADGM is associated with a friendly regulatory environment and fintech-oriented efforts.

- Virtual Assets: If your business involves crypto or digital tokens, Dubai’s VARA (Virtual Assets Regulatory Authority) issues the license, while the UAE Central Bank covers dirham-pegged stablecoins.

Step 2. Select your business structure

Most founders prefer a Limited Liability Company (LLC) for flexibility and investor appeal. Review your ownership needs and funding plans before finalizing.

Step 3. Prepare documentation

Have your documents ready in advance. Typical requirements include:

- Business plan with financial forecasts

- Technology and cybersecurity framework

- Compliance policies (AML, data protection, etc.)

- Management team profiles and CVs (fit and proper test)

- Proof of funds and their source

- Business continuity and governance policies

Step 4. Apply for your license

Submit your application to the right authority:

- DFSA for DIFC companies

- FSRA for ADGM companies

- Central Bank of the UAE for certain mainland activities

- VARA if you deal with virtual assets

Step 5. Register your company

Once approvals are in place, complete formalities like company name reservation, constitutional documents, initial approvals from the chosen free zone or mainland authority, and trade license.

Step 6. Secure office space

DIFC requires a physical presence, usually within its district. ADGM offers more flexibility, with options ranging from shared workspaces to virtual offices for startups.

VARA requires a registered office within the Dubai World Trade Centre (DWTC) free zone.

Step 7. Open a bank account

Banking can be challenging for fintechs. Apply early and approach multiple banks. Success improves if you have transparent compliance systems, clear source of funds, experienced management team, and strong AML/KYC policies.

Step 8. Build your team

Some of the crucial recruits to consider include compliance officers, risk managers, and tech specialists. It is easier to attract global talent through programs such as the Dubai Golden Visa.

Step 9. Set up technology infrastructure

Invest in secure, scalable systems that meet regulatory standards. The initial priorities should be on cybersecurity, data protection, and payment and banking system integration.

Step 10. Test in a sandbox

Both DIFC and ADGM also provide regulatory sandbox models where fintechs are able to pilot solutions with actual users. Admission requires demonstrating innovation and risk controls. To obtain complete approval, results should be documented.

Step 11. Launch and scale

After approvals, you can go to market. Sustainable growth depends on balancing innovation with strict compliance. Long-term success also requires regulatory reporting, consumer protection policies, cybersecurity audits, and responsible marketing (VARA has strict rules for digital assets).

How much does it cost to setup a fintech company in Dubai?

Budgeting fantasies don’t build successful companies, so let’s examine the real numbers.

| License Type | Main Costs | Estimated First-Year Cost (2025) |

|---|---|---|

| DIFC Innovation License (Startup Entry) | • License Fee: ~AED 5,500 (subsidized) • Office Space: AED 20,000–40,000 (basic) or AED 150,000+ (premium) • Legal & Setup: AED 30,000–60,000 | AED 70,000–250,000* |

| ADGM Fintech / RegLab Package | • Application Fee: AED 5,500 • License Fee: AED 5,000–20,000 • Setup: AED 40,000–80,000 | AED 60,000–120,000* |

| Full Financial Services License | • License Fee: AED 100,000–500,000 • Capital: AED 500,000–10M • Setup & Compliance: AED 200,000–400,000 • Marketing: AED 200,000–800,000 | AED 1M–12M* |

Hidden costs can derail budgets:

- Banking relationships require AED 20,000-55,000 in relationship fees.

- Compliance officers command AED 220,000-440,000 annually.

- Technology infrastructure setup costs AED 100,000-400,000.

- Audit requirements add AED 20,000-75,000 annually.

These expenses often catch entrepreneurs off-guard but are essential for successful operations. Factoring hidden costs is critical for a fintech company in Dubai to avoid roadblocks. Not sure about your setup cost? Use our Cost Calculator to get an instant estimate.

What is the process timeline for setting up Fintech in Dubai?

Starting a fintech company in Dubai usually takes between 12 and 18 months, depending on complexity, activities, licensing type. Though it can stretch longer if extended testing is needed. The first month is spent on groundwork, including preparing the business plan, selecting the right jurisdiction, and gathering necessary documents. The application stage follows, taking three to four months as regulators review submissions and issue in-principal approvals.

Once approvals are underway, the setup phase begins, which includes incorporating the business, opening a bank account, securing office space, and processing team visas. After that comes the regulatory sandbox, where products are tested with real users. This stage can last anywhere from six months to two years, depending on the complexity of the solution.

Finally, after successful sandbox testing, companies receive their full license and can officially launch and scale operations.

What are the compliance requirements that actually matter?

Compliance isn’t just about checking boxes but building trust with regulators, customers, and investors. For a fintech company in Dubai anti-money laundering requirements include customer due diligence procedures, transaction monitoring systems, suspicious activity reporting, and regular staff training.

- Risk Management Framework encompasses operational risk controls, cybersecurity protocols, business continuity planning, and regular risk assessments.

- Data Protection Standards cover UAE Data Protection Law compliance, international data transfer protocols, customer privacy safeguards, and breach notification procedures.

- Governance Requirements involve board composition standards, senior management oversight, internal audit functions, and regular regulatory reporting. Smart companies don’t see compliance as a burden but use it as a competitive advantage. Robust compliance builds customer trust and opens doors to partnerships that less compliant companies cannot access.

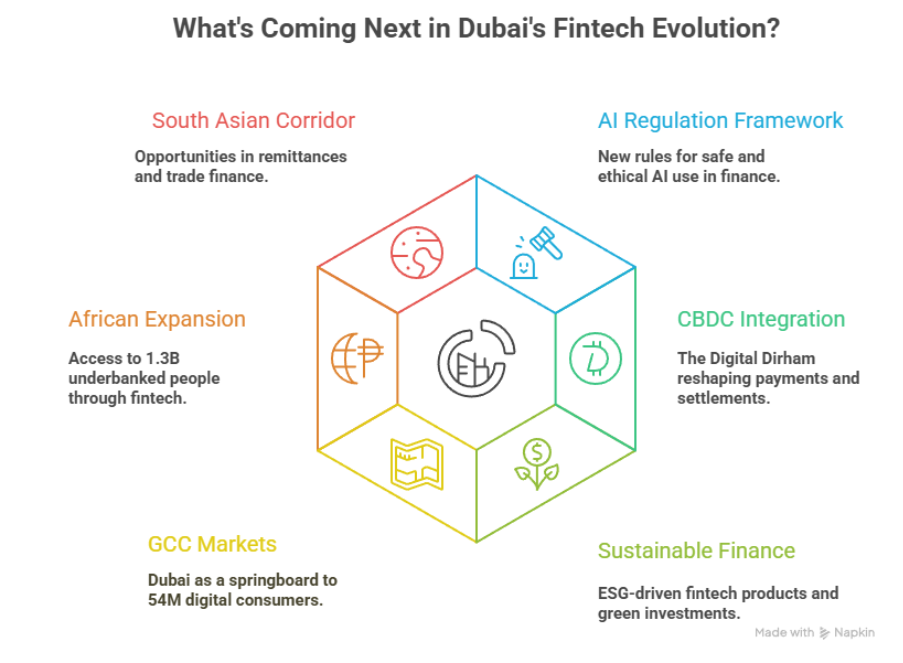

What did the Dubai Fintech Summit 2025 reveal about market direction?

The Dubai Fintech Summit 2025, held on May 12-13 at Madinat Jumeirah, offered a clear window into where the industry is heading. With thousands of business leaders, investors, and policymakers from over 120 countries in attendance, the summit reinforced Dubai’s position as a global hub for fintech innovation.

This year’s theme, “Fintech for All,” placed emphasis on inclusion and accessibility, while highlighting the sectors set for rapid growth. Digital payments remain the strongest segment, while embedded finance, integrating financial services into everyday platforms is fast becoming mainstream. Islamic fintech also stood out, with discussions focused on delivering Sharia-compliant solutions to tap into one of the world’s largest underserved markets.

Another area gaining momentum is insurtech, reflecting how insurance technology is becoming central to the region’s fintech evolution. Cross-border payment solutions also took center stage, showcasing how the Middle East is building more seamless and compliant systems for global transactions.

The summit further aligned with the UAE’s wider digital transformation agenda. Initiatives such as the Digital Dirham central bank digital currency project, the blockchain strategy aimed at digitizing 50% of government transactions, and Smart Dubai 2025 with its AI-powered services were highlighted as national priorities. Companies working within these frameworks benefit from faster regulatory approvals, stronger support, and early access to pilot programs.

Overall, the event made it clear: the next wave of fintech growth in Dubai will be defined by regulatory innovation, cross-border integration, and inclusive digital finance models.

Conclusion

Ready to turn your fintech vision into reality? The opportunity window remains open for starting a fintech company in Dubai, but competition will intensify, and costs will rise as more companies discover UAE advantages. Winning companies share three characteristics: they started with a clear regulatory strategy, chose the right jurisdiction for their business model, and invested in relationships alongside compliance.

Dubai’s regulatory framework, government support, and strategic location create unprecedented opportunities for companies ready to seize them. Success requires more than ambition but demands expertise, local knowledge, and strategic guidance from day one.

The next few months could determine whether you’re watching Dubai’s fintech boom from the sidelines or leading it from the center. Analysis paralysis costs opportunities, and the fintech companies launching in Dubai today will be tomorrow’s industry leaders.

Need expert guidance navigating Dubai’s fintech landscape? Our team will help you, fintech companies, successfully establish and scale in the UAE. From regulatory strategy to launch execution, we turn complex processes into competitive advantages.