Every year, countless entrepreneurs delay or abandon UAE expansion plans due to confusion about Corporate Tax, VAT, and Excise Tax requirements, turning opportunities into costly setbacks. These form the backbone of the UAE’s low-tax system.

For businesses and entrepreneurs planning to setup their businesses in 2026, understanding UAE tax structure is essential for ensuring compliance in their operations. This blog covers these taxes and the necessary compliance requirements in detail.

What is corporate tax and how does it work in the UAE?

Corporate tax in the UAE is a direct tax on business profits. It is administered by the Federal Tax Authority (FTA). Taxable income of the businesses is calculated after deducting all the expenses including depreciation and loses.

This supports growth of non-oil GDP and complies with OECD’s Base Erosion and Profit Shifting standards.

Corporate tax varies according to the taxable income of the company as stated below:

- 0% on taxable income up to AED 375,000

- 9% corporate tax on taxable income exceeding AED 375,000

Domestic Minimum Top-up Tax (DMTT) is applied to constituent entities that are the members of large MNEs operating in UAE with global revenue over~ AED 3.15 billion. A DMTT ensures a 15% global minimum effective rate under OECD Pillar Two. It is effective since 1 January 2025.

| Income Band | Rate | Notes |

|---|---|---|

| AED 0-375,000 | 0% | Supports SMEs and startups |

| Above AED 375,000 | 9% | Standard rate across Emirates |

| MNE Minimum (Pillar Two) | 15% | Applies to large MNEs only |

Who must pay corporate tax in the UAE?

Corporate tax is applicable to all “Taxable Persons” in the UAE. This includes:

- Companies based in the UAE and other legal entities that are incorporated or effectively managed and controlled in the UAE.

- Foreign business entities with permanent establishment in the UAE.

- Natural persons or individuals, who conduct a business activity in the UAE and their turnover is more than AED 1 million.

What are the exemptions and reliefs for UAE corporate tax?

Some businesses are exempt from corporate tax, because of their importance and contribution to society. These exemptions include the following entities:

- Government owned or government-controlled entities

- Small business relief (SBR)

- Qualifying Free Zone persons

What are penalties for non-compliance with the UAE corporate tax?

There are certain penalties under the UAE corporate tax law, which includes:

Late Registration: A penalty of AED 10,000 is imposed for failing to submit a registration application within the FTA’s timeframe.

Late Filing of Tax Returns: A fine of AED 500 per month, applies for the first 12 months, that can be increased to AED 1,000 per month for the 13th month onward.

Late Payment: Late payment of corporate tax attracts a penalty of 14% per annum on the unpaid amount.

Failure to Keep Records: If businesses do not maintain records, then a fine of AED 10,000 is charged, which may increase to AED 20,000 if there is a similar issue within 24 months.

Incorrect Filing: If there is any incorrect filing, then a fine of up to AED 20,000 is charged.

Navigating UAE Tax Regulations?

Get Our UAE Tax Compendium

Download Free Guide ↗How value added tax (VAT) works in the UAE?

Value Added Tax is an indirect consumption tax which is applied on the value added to goods and services at each stage of production and distribution. It is applied at a standard rate of 5%. The Federal Tax Authority is responsible for its regulation and collection. It is managed through their online portal EmaraTax.

This tax is collected from the end consumer in a business (output tax) and paid to the government. Usually, businesses can claim back the VAT paid on eligible business purchase (input tax).

There are two types of VAT registrations:

Mandatory registration is for the resident businesses in UAE, if their annual turnover of the company exceeds AED 375,000 or it is expected to exceed this threshold within the next 30 days.

Voluntary registration can be opted if the company turnover is less than the mandatory threshold, but the turnover should exceed AED 187,500 over the past 12 months or is expected to do so in 30 days.

What are obligations of VAT registered businesses?

The obligations for VAT registered businesses are mentioned below:

- Maintain a proper set of commercial records that allows government to verify the accuracy of their transactions.

- They must charge VAT on taxable goods and services they supply.

- May reclaim any VAT they have paid on business-related goods or services.

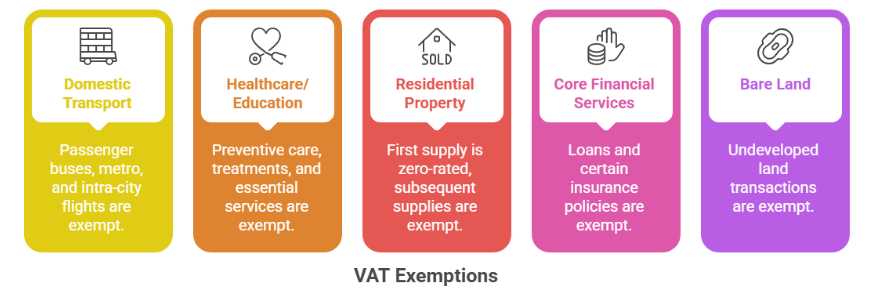

What are the VAT exemptions in the UAE?

Here is a list of common VAT exempt goods and services:

- Transportation: Domestic passenger transport, including intra-city flights, metro services, buses and local public transport. However, international transportation, like air and sea travel falls under zero-rated supplies in UAE.

- Healthcare and Education: Services like preventative care, treatments and essential medical services.

- Residential properties: Sales and rental of residential buildings are VAT exempts in UAE after the first supply. However, they are subject to standard VAT rate. The first supply of residential properties is zero-rated, which allows developer to recover input VAT.

- Financial services: Services like interest on loans and certain insurance policies that do not involve an explicit fee or return. But financial services that charge a clear fee, like banking and investment advisory services, may be subject to VAT.

- Bare land: Transactions including undeveloped land.

What is excise tax and how it works in the UAE?

Excise tax is a form of indirect tax which was introduced in 2017 across UAE. It is levied on certain goods which are typically harmful to human health or the environment, these goods are referred as “excise goods”.

Below is the list of products with their respective tax rates:

| Products | Rate of Excise Tax (%) |

|---|---|

| Tobacco and tobacco products | 100 |

| Liquids used in electronic smoking devices and tools | 100 |

| Electronic smoking devices and tools | 100 |

| Carbonated drinks (excluding sparkling water) | 50 |

| Energy drinks | 100 |

| Sweetened drinks | 50 |

The UAE government levies excise tax to reduce consumption of unhealthy and harmful products.

Who needs to register for excise tax?

Under the UAE Federal Decree Law NO. 7 of 2017 on Excise tax, businesses which are involved in any of the activities mentioned below, must register for excise tax.

Activities under excise tax includes:

- The import of excise goods in UAE

- The production of excise goods, from where they are supplied for consumption in the UAE

- The stockpiling of excise goods in the UAE in certain cases

- Anyone who has the responsibility to oversee and excise warehouse or designated zone (a warehouse keeper)

Conclusion

UAE tax structure mainly consists of three types of taxes, Corporate Tax, Value Added Tax (VAT) and Excise Tax. Corporate tax is a form of direct tax levied on income or profit of the company. It is 0% up to a threshold of AED 375,000 taxable income and 9% above that.

While VAT is an indirect consumption tax which is applied to goods and services at a rate of 5%. Excise tax is an indirect tax levied on certain which harmful to health or nature.

It is very important for a company to comply with the tax structure to build its reputation and ensure growth in the IAE. However, it is very challenging for a company to manage its tax structure alongside its business operations. With the help of Stratrich Consulting, you can be sure the process is hassle-free.