The UAE will introduce an e-invoicing system in July 2026 that will be mandatory. The introduction of e-invoicing has left a lot of business owners with some problems. Perhaps you have received emails from your accounting software provider, or your finance team has flagged upcoming deadlines.

Questions are increasing: Will our current systems handle structured invoices? How much will implementation cost? What happens if we miss the deadline?

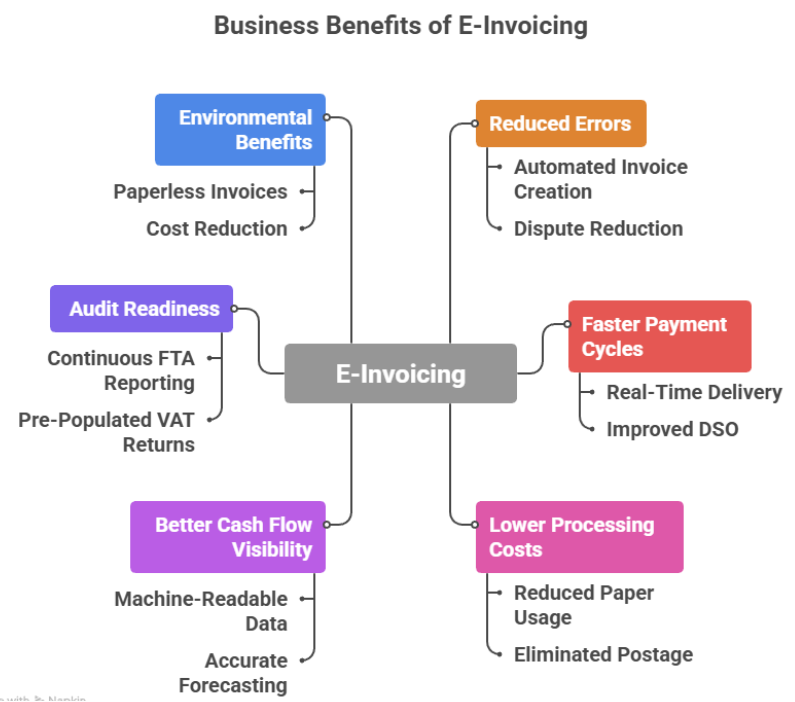

You’re not alone. With the Federal Tax Authority introducing the Electronic Invoicing System starting 1 July 2026, every VAT-registered business in the UAE will soon face this transformation. However, proper preparation now can unlock significant opportunities. Businesses that act early will streamline invoicing processes, reduce errors by up to 35%, accelerate payment cycles, and gain competitive advantages through automation.

This blog explains exactly how to navigate e-invoicing in the UAE, including the financial regulations, whether you operate under a mainland or Free Zone licence

What is the new e-invoice regulation in the UAE?

E-invoicing in the UAE is a mandated system designed for generating, exchanging, and securely storing invoices in a government-approved digital format such as XML, which must be electronically submitted to the Federal Tax Authority (FTA).

The implementation requires the use of an approved service provider, with the mandatory rollout starting on July 2026.

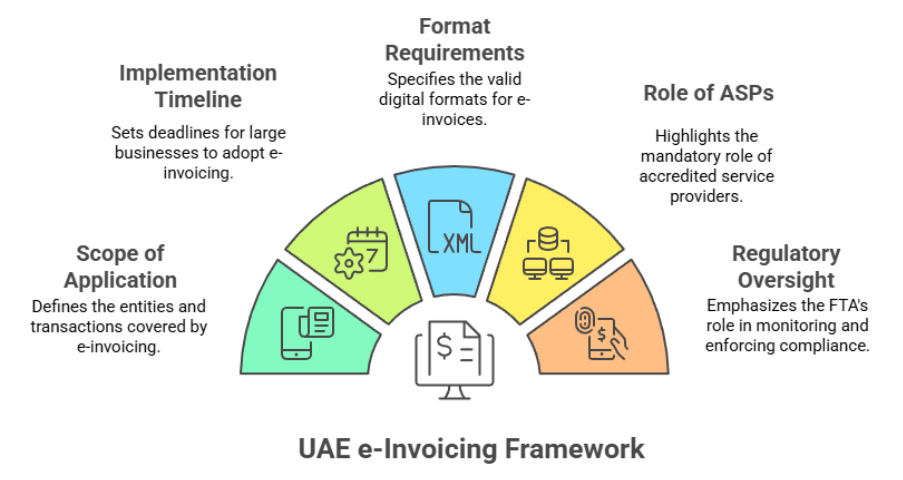

What is the UAE’s e-invoicing framework?

The UAE Ministry of Finance outlined a specific framework for the same through Ministerial Decisions No. 243 and 244 of 2025. Key requirements for valid e-invoices:

For digital formats, XML or JSON, employing recognized standards such as UBL (Universal Business Language) or PINT Peppol Invoice Standard

Through Accredited Service Providers (ASPs) that are approved by the Ministry of Finance.

Reports shall be submitted to the Federal Tax Authority no later than on the fourteenth day following the day of the transaction date.

Storage that is secure for no less than five years with integrity and accessibility maintained.

Compulsory Data Fields: All e-invoices and credit notes shall contain the data fields prescribed by the Ministry, which include but are not limited to seller and buyer details, VAT numbers, tax breakdowns, unique invoice identifiers, and transaction dates.

System Failure: In case of any system failure, businesses should report to the Federal Tax Authority within two business days using the defined procedures.

Electronic credit notes shall be issued and transmitted using the same format and system utilized for invoices and shall reflect cancellations or adjustments.

Scope and phasing: e-invoicing applies to most B2B and B2G transactions, with phased mandatory implementation based on business size and sector. Currently, B2C transactions are excluded.

*Note: Paper invoices in traditional form, PDFs, scanned copies, and Word documents will not constitute valid e-invoices.

The UAE has adopted the Peppol-based Decentralised Continuous Transaction Control and Exchange (DCTCE) model, also known as the 5-corner model, wherein ASPs perform data validation of invoices between parties whilst reporting the respective data directly to the tax authority.

What is the implementation timeline for e-invoicing in the UAE required for your business compliance?

The rollout follows a phased approach based on company size:

Phase

Business Category

ASP Appointment Deadline

Go-Live Date

Pilot

Taxpayer Working Group

30 June 2026

1 July 2026

Phase 1

Revenue ≥ AED 50 million

31 July 2026

1 January 2027

Phase 2

Revenue < AED 50 million

31 March 2027

1 July 2027

Phase 3

Government entities

31 March 2027

1 October 2027

Any business may voluntarily adopt e-invoicing from 1 July 2026, providing competitive advantages through improved efficiency before the mandate applies.

Who must comply with e-invoicing in the UAE?

E-invoicing applies to all VAT-registered entities conducting business-to-business (B2B) and business-to-government (B2G) transactions. This includes both mainland companies and Free Zone establishments.

Transactions that are currently excluded are:

Business-to-consumer (B2C) transactions (may be included later)

Government sovereign activities not competing with the private sector

International passenger air transport with electronic tickets

International goods transport by air with airway bills (24-month exemption)

VAT-exempt or zero-rated financial services

Transactions determined exempt by the Minister of Finance

*Note: Financial institutions within the Dubai International Financial Centre (DIFC) follow separate frameworks and are currently exempt.

Step-by-Step compliance roadmap for UAE e-invoicing

Start with a thorough audit of your current invoicing setup. Find all the systems that create invoices, including ERP platforms, accounting software, point-of-sale systems, or custom solutions, and assess their ability to produce structured XML or JSON outputs.

Most businesses find that manual PDF creation or outdated systems need significant improvements. Document the following:

Current monthly invoice volume

Types of transactions: B2B, B2G, cross-border

Customer base and their technical readiness

Integration points between different business systems

Current data storage and archiving methods

This assessment serves as the basis for your implementation plan and budget needs.

Step 2: Select an Accredited Service Provider

Only ASPs approved in advance by the UAE Ministry of Finance can transmit and validate e-invoices. In November 2025, a list of approved providers was released by the Ministry. Such an ASP should be Peppol-certified and should have a minimum of two years of operational experience in e-invoicing systems.

When selecting an ASP, consider:

Integration capabilities with your existing ERP or accounting software

Experience serving businesses in your industry sector

Pricing structure and ongoing support provisions

Data security measures and ISO certifications

Availability of training and implementation assistance

VAT groups require each member to establish separate endpoint connections with their ASP whilst using the group’s Tax Registration Number.

Step 3: Upgrade your technology infrastructure

Your systems must generate invoices with all required fields listed in the UAE e-invoicing data dictionary. Key elements include:

Unique invoice identifier following sequential numbering

Invoice issue date and time in the required format

Supplier and buyer details, including Tax Registration Number (TRN)

Detailed line items with descriptions, quantities, unit prices, and tax rates

Tax calculations broken down by rate category

Total amounts including and excluding VAT

Payment terms, methods, and bank details

Digital signatures or electronic seals where required

Technology upgrade options:

Native ERP modules: If your ERP provider has e-invoicing functionality, then this typically provides the most seamless integration.

Middleware solutions: Legacy system integration into modern e-invoicing platforms-without changing the whole system.

Cloud-based platforms: Adopt new cloud accounting systems with built-in e-invoicing compliance.

Custom development: Build bespoke solutions for unique business requirements.

Budget sufficiently for software licenses, implementation services, data migration, and system testing. The Ministry of Finance estimates that automation through e-invoicing can decrease invoice processing costs by up to 66%.

Step 4: Ensure data quality and mandatory fields

E-invoicing in the UAE requires precise, structured data. Non-compliant invoices will be rejected by ASPs or the Federal Tax Authority, causing operational disruptions and possible penalties.

Important data requirements:

Tax Registration Number (TRN): Must be valid and active for both supplier and buyer.

Invoice numbering: Sequential, unique identifiers with no gaps in the sequence.

Date formats: ISO 8601 standard (YYYY-MM-DD).

Currency codes: ISO 4217 standard (AED for UAE Dirhams).

Tax classifications: Correct standard, zero-rated, or exempt categorisation.

Unit of measure codes: Standardised codes for quantities.

Implement data validation rules within your systems prior to invoices reaching your ASP. Detecting errors early helps avoid rejection and reprocessing expenses.

Step 5: Train your finance team

E-invoicing represents a fundamental shift in invoice processing. Your team needs training on:

New invoice creation workflows through your ASP platform

Data validation requirements before transmission

Correction procedures (issuing electronic credit notes for errors)

System failure protocols (must notify FTA within two business days)

Record-keeping obligations and audit preparation

Consider appointing an internal e-invoicing champion who becomes an expert in the system and serves as first-line support for colleagues.

Step 6. Test before go-live

Use the pilot phase starting July 2026 to conduct testing even if you’re not in the Taxpayer Working Group. Many ASPs offer sandbox environments where you can practice creating, validating, and transmitting test invoices without impacting production systems.

Testing should cover:

End-to-end invoice workflows from creation to FTA reporting

Integration between your ERP system and ASP platform

Error handling and rejection scenarios

Volume stress testing (can your system handle peak transaction periods?)

Cross-border transactions with international customers

Step 7: Establish robust record-keeping

The Tax Procedures Law mandates keeping invoice data for five years, or 15 years for real estate transactions. Implement secure archiving solutions that ensure data integrity, tamper-proof storage, and easy retrieval for audits. Your ASP usually offers archiving services but verify that storage locations and data sovereignty comply with UAE regulations. Regular backups and disaster recovery procedures are crucial.

What penalties and compliance risks are associated with UAE e-invoicing?

The UAE applies its existing VAT penalty regime to e-invoicing violations under Cabinet Decision No. 49 of 2021:

Failure to issue proper tax invoice: AED 2,500 first instance, AED 5,000 for repeat violations.

Failure to maintain proper records: AED 10,000 first offence, AED 20,000 for repeat cases.

Incorrect reporting or transmission failures: Penalties mirror VAT non-compliance fines.

More worrying than fines, however, is the fact that non-compliant invoices will be rejected for claims of VAT credit. If your invoices do not conform to e-invoicing standards, customers cannot recover input VAT, thereby harming business relationships and competitive positioning.

The Federal Tax Authority can also charge extra penalties for the following:

Providing false or misleading information

Obstructing FTA inspections or audits

Failing to notify system failures within two business days

Operating without a valid ASP connection after your deadline

Managing cross-border and international transactions

E-invoicing applies to transactions with overseas customers, though implementation differs based on Peppol network participation.

For Peppol-connected international buyers: Use their existing Peppol address for seamless invoice exchange through the network. This provides instant delivery confirmation and automated processing on the buyer’s side.

For non-Peppol foreign customers: Your ASP still reports the invoice to the FTA within 14 days, but you transmit the invoice outside the network (typically via email) whilst maintaining the structured XML version for compliance.

All e-invoices must comply with UAE PINT framework requirements regardless of customer location. The 14-day FTA reporting obligation applies to all transactions within scope, whether domestic or international.

How is UAE e-invoicing supporting SMEs in digital transformation?

The UAE Ministry of Finance recognises that 82% of UAE businesses are micro businesses with less than AED 3 million annual turnover. As of mid-2022, the UAE had 557,000 SMEs, contributing 63.5% to non-oil GDP.

The phased implementation provides smaller businesses additional time until July 2027, allowing them to learn from early adopters. SMEs benefit from:

Level playing field with larger enterprises through standardised processes

Access to affordable ASP services enabling automation

Automatic pre-population of VAT return fields

Expedited refund processing through real-time data

Seamless participation in international Peppol network

Conclusion

UAE e-invoicing represents the most significant financial compliance change since VAT introduction in 2018. Success requires more than just technology; it demands process redesign, team training, and strategic planning.

Businesses that view e-invoicing as an opportunity rather than a burden will realise substantial benefits beyond compliance: streamlined operations, reduced costs, faster payments, and better financial visibility. The key is starting now, whilst you still have time for thoughtful implementation rather than rushed crisis management.

Whether you’re a Phase 1 business facing January 2027 deadlines or a smaller enterprise with until July 2027, the preparation steps remain consistent. Select your ASP carefully, invest in proper systems, train your teams thoroughly, and test comprehensively. These foundations ensure seamless compliance when your deadline arrives and position your business for success in the UAE’s digital economy.