For any VAT-registered business in the UAE, two figures define each tax period: output VAT and input VAT. Output VAT (VAT payable) is what the business owes the Federal Tax Authority (FTA) from its sales. While the input VAT (recoverable VAT) is what the business can reclaim on its purchases. The difference between the two shows whether the business needs to pay VAT to the FTA or just a refund, for that period.

Understanding how to calculate both correctly, which items fall outside the standard rules, and where the law places hard limits on recovery is not optional. It is the core of day-to-day VAT management.

This guide explains how output VAT is calculated and adjusted, how input VAT recovery works, what blocks it, and the specific VAT treatments that apply to commercial real estate, deposits, and compensation payments.

Navigating UAE Tax Regulations?

Get Our UAE Tax Compendium

Download Free Guide ↗How Output VAT is Calculated

Output VAT is the total VAT a business must pay during a tax period. It includes more than just standard-rated sales; other transactions can also create an output VAT obligation.

The calculation of Output VAT is as follows:

| A. | Standard-rated Sale at 5% | XX |

| B. | Deemed Supplies | XX |

| C. | Goods took for own use and the gift of goods | XX |

| D. | Discounted Sales | XX |

| E. | Delivery Charges & Service Charges | XX |

| F. | Bad Debts relief | (XX) |

| Total Output VAT (A + B+ C + D + E – F) | XXX | |

1. Standard-Rated Sales

VAT at 5% applies to all supplies that are not exempt, zero-rated, or out of scope. These form the largest component of output VAT for most businesses.

2. Deemed Supplies

A deemed supply arises even where no consideration is received. The two main triggers are:

- Some or all of a taxable person’s assets are supplied for no consideration

- Goods and services are held by a taxable person at the date of VAT deregistration

Gifts are treated as deemed supplies only where the value of Gift exceeds AED 500 to each recipient and total output VAT across all such gifts within a 12-month period reaches AED 2,000 or more. Only the amount exceeding AED 2,000 is payable. For supplies between government entities or charitable organisations, the threshold is AED 250,000, and only the excess above that amount is due.

3. Goods Taken for Own Use

When a trader takes goods from stock for personal use, they must pay output VAT based on the cost or value of the goods, provided input VAT was originally claimed. This ensures the personal use of goods on which input VAT was recovered is brought back into the output VAT position.

4. Discounted Sales

VAT in UAE always payable on the actual price paid by the customer. Any discount given to the customer should be deducted from total price before calculating the VAT Output. However, in case of Cash Discount the supplier has two options of calculating the Output VAT amount.

For cash or prompt payment discounts, the supplier has two options:

- The supplier should issue the invoice for the full VAT amount. If the customer pays on time and takes the discount, issue a credit note to reduce the output VAT.

- Include both the discounted and non-discounted values on the invoice to clarify that the taxpayer can claim VAT only for the value they paid for the goods purchased.

In case of using the discount option, the seller must adjust their accounts by registering the output tax.

5. Delivery and Service Charges

Delivery charges and service charges form part of the consideration for the principal supply. Where goods cannot be supplied without delivery, the delivery charge is not treated as a separate supply. Its VAT treatment follows the same as VAT treatment of the goods being delivered.

6. Bad Debt Relief

According to UAE VAT law, the supplier must charge VAT even before the client pays for the goods or services provided. If the client fails to pay, and the debts cannot be recovered, then a bad debts allowance can be made.

To claim this relief, all four of these conditions must be satisfied under Article 64:

- The supplier has already issued a proper tax invoice, declared the VAT on their return, and paid it to the FTA.

- The debt is at least six months overdue from the date of supply

- The debt has been formally written off in the supplier’s accounting records

- The supplier has notified the customer in writing of the exact amount of consideration written off

Bad debt relief is claimed as a negative adjustment in the VAT return for the period in which all conditions are satisfied. When a supplier claims relief, the customer, if VAT-registered, is simultaneously required to reverse the corresponding input VAT previously claimed.

Adjusting Output VAT

Output VAT adjustments are made through two formal documents:

- A Tax Credit Note is issued where output VAT needs to be reduced, for example following a return, a cancellation, or a bad debt relief claim

- An Additional Tax Invoice is issued where output VAT needs to be increased, for example where additional consideration is agreed after the original supply

VAT on the Sale of Commercial Real Estate

The sale of commercial property in the UAE is a standard-rated supply at 5%. However, a specific process called the Special Payment Mechanism (SPM) applies in certain transactions.

Where commercial property is sold by any supplier other than the original developer, the buyer must pay the 5% VAT directly to the FTA before the Land Department processes the title transfer. The buyer pays through the Emara Tax portal or an FTA-nominated bank and receives a Payment Transaction Number (PTN) as proof. That PTN must be presented to the Land Department to complete ownership transfer. The seller still issues a normal tax invoice and declares the output VAT in their own VAT return.

The SPM does not apply in the following situations:

- Sales or leases of residential properties

- Leases of commercial properties

- Sales of commercial properties by the original developer

- Sales of commercial properties with existing tenants to a VAT-registered buyer, where the transaction qualifies as a Transfer of a Going Concern (TOGC)

In all these cases, the seller collects VAT in the normal way and remits it through their own VAT return.

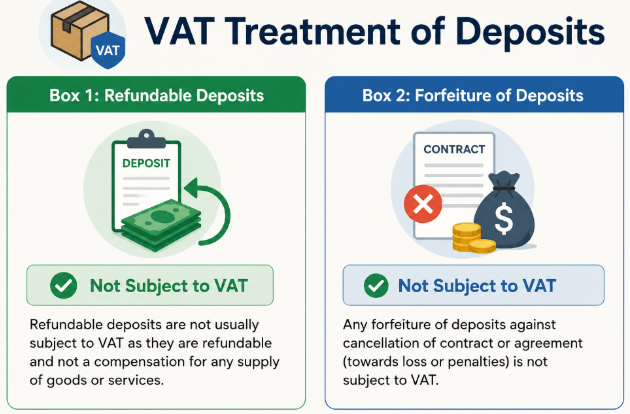

VAT on Deposits and Compensation Payments

The VAT treatment of deposits and compensation payments depends on whether the payment relates to a supply of goods or services or acts purely as an independent penalty.

| Payment Type | VAT Treatment |

|---|---|

| Refundable deposit | Not subject to VAT |

| Forfeited deposit for cancellation of a reservation/service | Not subject to VAT |

| Forfeited deposit for non-payment on a completed supply | Subject to VAT |

| Hotel deposit forfeited on cancellation | Subject to VAT |

| Non-refundable deposit | Subject to VAT |

Refundable deposits are not taxed because they are not payment for goods or services. If a deposit is lost because of a cancellation or as a penalty, it is also not taxed, since it does not relate to a sale. However, if a deposit is lost because a customer did not pay for goods or services already received, then it counts as sale and thus taxes are applied on it.

Hotels that keep deposits after cancellations are an exception: those deposits are taxed regardless of the usual rule. Non-refundable deposits are considered part of the payment for a sale and are taxed from the start.

How Input VAT Recovery Works

Input VAT is the VAT a business pays on its purchases. Where those purchases are used to make taxable supplies, the VAT is recoverable from the FTA, either as an offset against output VAT or as a net refund.

| A | Standard-rated Expenditure at 5% | XX |

| B | Entertainment | XX |

| C | Gift | XX |

| D | Purchase of Car | XX |

| Total Input VAT (A – B – C – D) | XXX |

Recovery is not automatic. All of the following conditions must be satisfied:

- The recipient must be a VAT-registered taxable person

- The recipient must hold a valid tax invoice from the supplier

- The goods or services must have been used for an eligible purpose, meaning to make taxable supplies in the UAE

- The recipient must have paid, or genuinely intend to pay, the full consideration within six months from the agreed payment date. Partial payment entitles the business to a proportionate recovery. If no payment is made, the full input VAT previously claimed must be reversed

- VAT must have been correctly charged by the supplier

- The input VAT must not fall within a blocked category

Eligible Purpose

Recovery of input VAT depends on if the purchased items are used for making taxable sales within your business. If part of the purchased item is used for taxable sales and other portions for non-taxable activities, input VAT should be apportioned accordingly. Only the portion attributable to taxable activities is recoverable.

Irrecoverable (Blocked) Input VAT

Certain categories of input VAT cannot be recovered under Article 53 of the VAT Executive Regulations. These restrictions apply to all businesses except designated government entities.

Entertainment

Input VAT on entertainment provided to anyone other than employees is not recoverable. This includes customers, potential customers, officials, shareholders, owners, and investors.

Employee entertainment is also blocked, with three exceptions:

- Such entertainment is required by Labour Law of UAE

- It is a documented contractual obligation forming part of normal business practice in employing those individuals

- It constitutes a deemed supply, such as a gift above the applicable threshold

- Regular consumables provided during the course of business, such as tea, coffee, and snacks at office meetings, are generally recoverable as they are considered a normal business cost rather than entertainment.

Gifts to Employees VAT is recoverable where:

- Required by Labour Law of UAE

- There is a contractual obligation

- It considered as deemed supply

- Regular expenses like tea, coffee, snacks in office or regular snacks in office meetings.

Special Rule: Health insurance for employee dependants

In accordance with the decision of the Cabinet No. 100, dated 2024, which took effect on 15 November 2024, the VAT on the supply of insurance cover for the dependants of the staff members can be recovered in respect of one spouse and up to three children aged under 18 years.

Motor vehicles

Input VAT on the purchase, rental, or lease of a motor vehicle available for personal use by any person is not recoverable. Three categories are excluded from this block:

- Licensed taxis

- Motor vehicles registered as emergency vehicles used by police, fire, ambulance, or other emergency services

- Vehicles rented to customers in a vehicle rental business

Input VAT on flat rate reimbursements paid to employees is not recoverable.

Adjustment of Input VAT

An adjustment of input tax once paid is allowed under the following conditions:

- Change of use from taxable use to non-taxable use.

- Change of use from non-taxable use to taxable use.

Time limit of recovering Input Tax

Input VAT must be recovered in the first tax period in which both of the following conditions are met:

- The tax invoice has been received by recipient

- The recipient has the intention to pay the full consideration within six months of the agreed payment date

A business may also recover input VAT in the tax period immediately following the period in which both conditions are first met. Recovery later on isn’t allowed unless you voluntarily disclose and correct the previous period, and penalties may apply.

Where payment is not made within six months of the agreed due date, the input VAT must be reversed. Once payment is eventually made, the input VAT can be recovered again in the period of payment.

Pre-Registration Input VAT Recovery

A business that registers for VAT may recover input VAT incurred before its registration date, subject to the following conditions:

| Type | Condition | Time Limit |

|---|---|---|

| Goods | Acquired for business purposes and still in stock on the registration date | No time limit |

| Services | Supplied for business purposes | Within 5 years prior to the registration date |

Input VAT on services incurred more than five years before the registration date cannot be recovered under any circumstances.

Conclusion

Output VAT and Input VAT are the two sides of every VAT return. Calculating output VAT accurately requires accounting for deemed supplies, own-use withdrawals, discount arrangements, delivery charges, and bad debt positions. Recovering input VAT correctly depends on meeting the payment intention condition, using goods and services for an eligible purpose, and identifying which expenses fall within the blocked categories.

For commercial real estate, deposits, and compensation arrangements, additional classification decisions arise before VAT is applied or withheld. Each of these has its own VAT ramifications that must be determined at the time of the transaction and cannot be determined afterward.

Firms that undertake regular VAT checks, especially given the new rules that are in effect since November 2024, are best placed to prevent overpaying VAT, missing out on legitimate tax savings, and incurring penalties.