Every VAT-registered business in the UAE faces the same foundational question with each transaction: which supply category does this fall under? The answer determines whether VAT is charged, at what rate, and whether the business can recover the VAT it paid on its own costs.

The UAE introduced VAT on 1 January 2018 through Federal Decree -Law No. 8 of 2017, to a standard rate of 5%. Not all supplies carry that rate, and not all supplies fall within the taxable framework at all. Under the FTA’s classification structure, every supply belongs to one of four categories: out of scope, exempt, zero-rated, or standard-rated.

Each category has different VAT obligations and input tax recovery positions. Getting the classification wrong creates compliance exposure. This guide covers all four supply types, what falls within each, and what the latest regulatory changes mean for businesses.

The UAE VAT Supply Framework

Before going into each category, it helps to understand the core logic. Supply classification does two things: it sets the output VAT rate charged to customers, and it determines whether input VAT on related costs is recoverable.

| 1. | Out of Scope Supplies | Non-Taxable Supplies | Not eligible for Input Tax Credit |

| 2. | Exempt Supplies | ||

| 3. | Zero Rated Supplies | Taxable Supplies | Eligible for Input Tax Credit |

| 4. | Standard Rated Supplies |

The distinction between exempt and zero-rated is the one that matters most in practice. Both result in no VAT charge to the customer but zero-rated supplies allow the supplier to reclaim all input tax, while exempt supplies do not. For businesses with significant operational costs, that difference has a direct impact on the bottom line.

Navigating UAE Tax Regulations?

Get Our UAE Tax Compendium

Download Free Guide ↗1. Out of Scope Supplies

Out of scope supplies fall entirely outside the UAE VAT system. They are not treated as supplies for VAT purposes, so no output VAT is due and no input tax on related costs is recoverable.

Under Article 7 of Federal Decree-Law No. 8 of 2017, the following transactions are out of scope:

- Salaries and employer-employee transactions: wages, benefits, and services performed by an employee in their capacity as an employee

- Transfer of a Going Concern (TOGC): where an entire business transfers as a going concern, provided the buyer is or becomes a taxable person and intends to continue the business (VATP015 applies)

- Charitable donations: genuine donations with nothing provided in return

- Tips in hotels or any other place

- Sale of vouchers at or below face value: any premium above face value is taxable at the standard rate (Article 7(1))

- Intra-group transactions within a VAT group: supplies between companies forming a single FTA-registered VAT group

- Temporary transfers to another GCC Implementing State: goods moved temporarily without a change of ownership

One-point businesses often overlook: Costs tied to out-of-scope activities carry no input tax recovery entitlement. Where a business has a mix of out-of-scope and taxable activities, input tax must be appointed accordingly.

2. Exempt Supplies

Exempt supplies sit within the UAE VAT framework but carry no output VAT obligation. No VAT is charged to the customer and, technically, no input tax is recoverable on directly related costs. This makes exemptions a real cost for businesses, as VAT incurred on related purchases becomes irrecoverable.

Article 46 of Federal Decree-Law No. 8 of 2017 defines four categories of exempt supply.

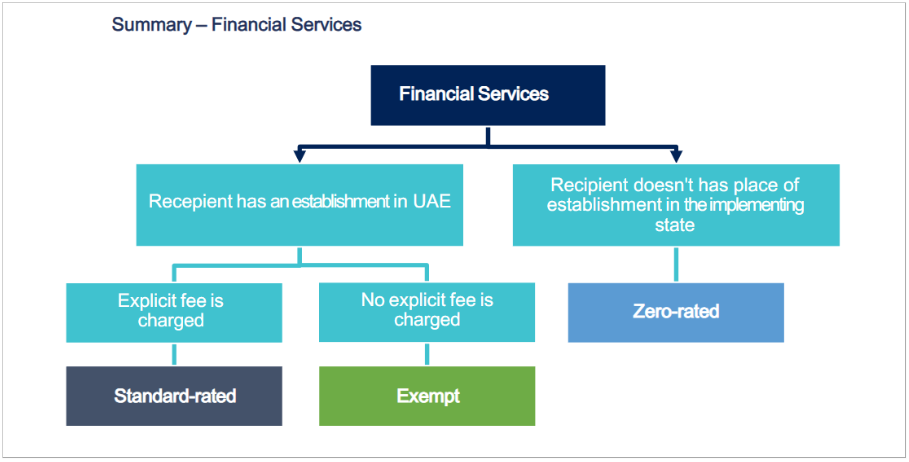

Financial Services

Financial services are exempt when supplied on a margin basis where income comes from the spread between a buying and selling price, not an explicit fee. This covers:

- Currency exchange

- Issue and transfer of debt and equity securities

- Loan and credit facility provision

- Operation of current, deposit, and savings accounts

- Financial instruments derivatives, options, swaps, and futures

- The payment or collection of interest, principal, dividends, or amounts relating to debt securities, equity securities, credit arrangements, or life insurance contracts

- Agreeing to undertake or arranging any exempt financial service transaction

The fee-versus-margin rule is critical: When any of the above services are supplied for an explicit fee, commission, discount, or rebate, they are no longer exempt they become standard-rated at 5%. The same financial transaction can carry different VAT treatments depending on how the supplier structures its pricing.

Two exceptions cross this line regardless of fee or margin:

- The issue, allotment, and transfer of equity or debt securities – always exempt

- Life insurance contracts and reinsurance of life insurance – always exempt

Reinsurance in any other context is standard-rated, except where it relates to an exported insurance service, which is zero-rated.

Where exempt financial services are supplied cross-border to a recipient outside the GCC Implementing States and the conditions for exported services are satisfied, the supply may qualify as zero-rated rather than exempt.

2024 updates – virtual assets and investment funds

Cabinet Decision No. 100 of 2024, effective 15 November 2024, extended the exemption for financial services in two important ways:

- The transfer of ownership and conversion of virtual assets (including cryptocurrencies) is retrospectively exempt from 1 January 2018. Services relating to safeguarding, managing, and enabling control of virtual assets are exempt from 15 November 2024. Crypto mining by an individual for their own account remains out of scope.

- Management of investment funds licensed by a competent UAE authority is exempt from 15 November 2024, under Article 42(2)(j) of the Executive Regulations. This covers fund operations management, investment management on behalf of the fund, and performance monitoring. Management of unlicensed funds and discretionary portfolio management are excluded.

Bare Land

The supply of bare land is exempt under Article 46. Key distinctions:

- Bare land with fencing – exempt

- Land used for irrigation – not bare land, standard-rated

- Land with any construction above ground level – loses bare-land status, exemption no longer applies

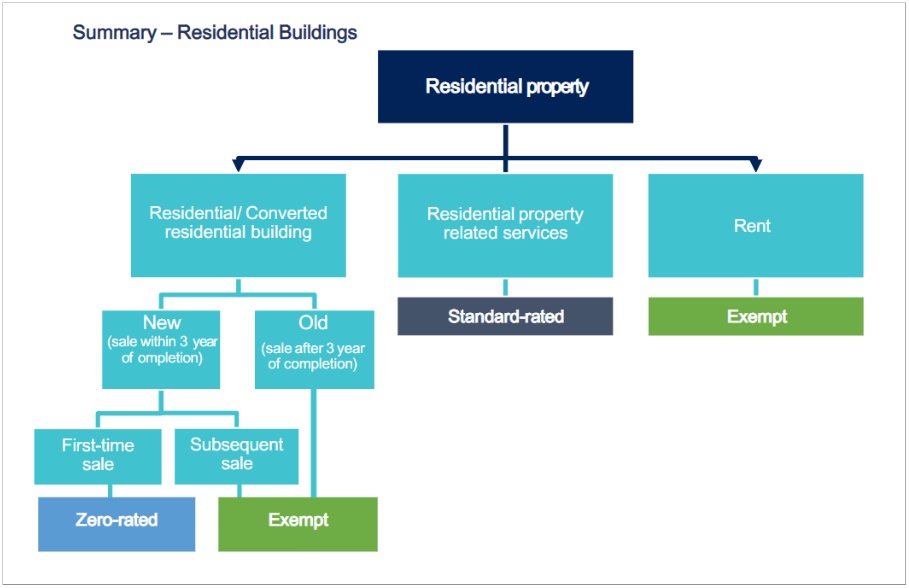

Residential Buildings

Residential buildings are generally exempt when sold or leased, with one exception handled under zero-rated supplies below. The definition of a residential building includes:

- Buildings occupied or intended to be occupied as a principal place of residence

- Student and school-pupil residential accommodation

- Orphanages, nursing homes, and rest homes

- Buildings where a small portion is used as office space

- Gardens, garages, and other areas adjoining or used in conjunction with the residential building form part of the residential building

The first supply of a residential building within three years of its completion is zero-rated rather than exempt. Subsequent sales or leases of the residential buildings are generally exempt. This distinction is important because zero-rated treatment allows recovery of related input tax, whereas exempt treatment does not.

The following do not qualify as residential buildings: hotels, motels, serviced apartments, bed and breakfasts, hospitals, and structures not fixed to the ground.

Local Passenger Transport

The transport of passengers by qualifying means of transport beginning and ending within the UAE is exempt, provided the journey is not for leisure or entertainment purposes.

Exemption applies only where the transport begins and ends within the UAE and does not form part of international carriage by air or sea. Pleasure trips, sightseeing tours, and transport primarily intended for entertainment or catering services do not qualify for exemption.

Qualifying means of transport includes:

- Motor vehicles (including taxis), buses, trains, trams, and monorails

- Ferryboats and helicopters used for public passenger carriage

Under Article 45 of the Executive Regulations, the passenger transport service carries no minimum capacity requirement for a single taxi qualifies. The ten-or-more-passenger threshold under Article 34(3) applies only to zero-rating the vehicle itself as a good, not the transport service.

School transport services are exempt as a service. The school bus itself, however, is standard rated at 5% when purchased or leased school buses serve a restricted user group and do not meet the public transport test for vehicle zero-rating.

3. Zero-Rated Supplies

Zero-rated supplies carry a 0% VAT rate. No VAT is charged to the customer, but unlike exempt supplies, the supplier retains full entitlement to recover input tax on all related costs. This frequently results in a net refund position from the FTA for businesses operating primarily in zero-rated sectors.

Article 45 of Federal Decree-Law No. 8 of 2017 and the Executive Regulations define the following zero-rated categories.

Educational Services

Zero-rated where all of the following conditions are met:

- The institution is recognised by the Federal or local government

- Services follow a government-recognised curriculum

- For higher education: more than 50% of funding comes from Federal or local government (Article 40(1)(b) ER)

- Printed and digital curriculum-related reading materials are also zero-rated.

The following are not zero-rated, even when supplied by a recognised institution:

- School uniforms

- Electronic devices

- Food and beverages

- Field trips

- Extracurricular activities

- Supplies to individuals not enrolled at the institution

Healthcare Services

Zero-rated if the supply has been made by an operator authorized under the Ministry of Health and Prevention or any other competent body in the UAE, provided that the supply is concerned with human well-being as recognized in the medical field. Also, pharmaceutical goods and medical instruments, as described under Cabinet Decision No. 56 of 2017, can be zero-rated.

Furthermore, goods used directly and necessarily while providing medical care to the patient are eligible for zero-rating.

Elective cosmetic procedures are standard-rated unless prescribed by a doctor to treat or prevent a medical condition (Article 41(3)(b) ER).

A critical B2B rule under FTA VATP016: zero-rating applies only where the recipient is the patient.

| Supply | VAT Treatment |

|---|---|

| Doctor → Hospital | Standard-rated at 5% |

| Hospital → Patient | Zero-rated at 0% |

| Laboratory → Hospital | Standard-rated at 5% |

| Laboratory → Patient (direct) | Zero-rated at 0% |

Exports of Goods and Services

The export of goods from the UAE is zero-rated. Following Cabinet Decision No. 100 of 2024, businesses can evidence zero-rating for exports made from 15 November 2024 with any of the following:

- Customs declarations alongside commercial evidence of export

- Shipping certificates with official supporting evidence

- Customs declarations confirming suspension status (for goods under a customs suspension regime)

Accepted official evidence also includes export certificates from local customs departments, clearance certificates from UAE authorities, or certified documents from the destination country’s authorities. All documents must carry official stamps or seals and be in Arabic or English or include a certified translation.

International Transportation

The following international transportation supplies are zero-rated:

- Passengers or goods transported from the UAE to a destination abroad

- Passengers or goods transported from abroad into the UAE

- Passengers transported within the UAE as part of an international journey

- Goods transported within the UAE as part of, or for the purpose of, transporting goods to or from a destination outside the UAE

- Insurance and arrangement of insurance or transport connected to international transactions

- The sale of goods on board aircraft or vessels during qualifying international transportation journeys is also zero rated

Domestic transportation services in the UAE, as part of an international trip, can be zero-rated only when the same provider renders both domestic and international transportation services. This has been stated under Article 33(1)(d) of the Executive Regulations, as amended by Cabinet Decision No. 100 of 2024, and FTA Public Clarification VATP040 (March 2025). However, if a different logistics company provides only domestic transportation services, it will be taxed at 5%.

First Supply of New Residential Buildings

The first sale of a newly constructed residential building within three years of construction completion is zero-rated. This allows property developers to recover input tax incurred during construction. After the three-year window, or on any subsequent sale, the supply becomes exempt and input tax recovery is no longer available.

First Supply of Charitable Buildings

The first sale of a charitable building within three years of construction is zero-rated. Subsequent sales and older buildings are standard-rated. The building must be used to advance the purposes of a government-approved and regulated charity and must not generate profit for owners, shareholders, or members.

Investment in Precious Metals

Gold, silver, and platinum of at least 99% purity, tradable in global bullion markets, are zero-rated. Cabinet Decision No. 127 of 2024, effective 25 February 2025, extended the domestic Reverse Charge Mechanism to palladium, diamonds, pearls, rubies, sapphires, emeralds, and predominating jewellery. Between registered businesses, the supplier invoices without charging VAT and the buyer self-accounts in their own VAT return. Any jewellery made from these precious metaslmetals are out of such zero rating and considered as standard rated supplies.

Crude Oil and Natural Gas

The extraction and supply of crude oil and natural gas is zero-rated under Article 45 of the Decree-Law. Petrol, LPG are not a natural gas and are considered as standard rated supplies.

Qualifying Means of Transport

Aircraft, sea vessels, and land-based means of transport used commercially for passengers or goods are zero-rated. Imports of qualifying transport are also zero-rated. Directly connected services repair, maintenance, and conversion are zero-rated provided the transport continues to meet qualifying conditions.

Qualifying land transport includes buses and trains used for mass public transportation, without restriction to a specific user group.

The following are not zero-rated:

- Transport restricted to a specific user group (school buses, private office vehicles)

- Peripheral services with only an indirect connection, such as cleaning a hangar

4. Standard-Rated Supplies

Standard-rated supplies are taxed at 5% and represent the default category any supply that does not fall into out of scope, exempt, or zero-rated is standard-rated. Input tax on costs related to standard-rated supplies is fully recoverable.

The majority of commercial goods and services in the UAE are standard-rated, including professional services, retail, advertising, hospitality, construction, commercial property, software, and domestic freight transport (where it does not form part of an international journey handled by the same supplier).

Healthcare services supplied business-to-business, non-qualifying educational supplies, domestic transportation services not linked to qualifying international transport, and most reinsurance services are also standard-rated.

Conclusion

Getting VAT supply classification right is one of the most consequential compliance decisions a UAE business makes. Charging VAT on a supply that should be exempt means over-charging customers and creating a liability the business does not owe. Treating a taxable supply as exempt means forfeiting recoverable input tax.

The four categories out of scope, exempt, zero-rated, and standard-rated each carry distinct obligations and consequences. With the FTA’s enforcement activity rising sharply and e-invoicing making supply-level data visible to regulators from mid-2026, the window for undetected classification errors is narrowing.

For any business making diverse supplies or operating in a sector affected by the 2024 Executive Regulation amendments financial services, virtual assets, healthcare, transport, or precious metals a structured review of current VAT treatment positions is a sound near-term priority.