The stakes have never been higher for businesses operating in the UAE. In the first half of 2025 alone, regulators imposed fines totalling over AED 42 million for anti-money laundering violations, with 1,063 businesses found to be in non-compliance. Whether you operate a real estate brokerage, an accounting firm, a gold trading business, or a corporate services company, authorities make it clear that compliance is mandatory.

Despite the challenging figures, there is real opportunity here. While some businesses face penalties and disruptions for non-compliance, those that take AML obligations seriously gain a clear edge. They secure stronger banking relationships, operate with greater credibility, and position themselves as dependable partners in the UAE market.

This blog explains what anti money laundering regulations in practical terms are, clarifies why anti money laundering is important for your success, and provides clear steps to ensure compliance.

What is the UAE anti-money laundering law?

To understand UAE anti-money laundering law, it’s important to first understand why it was implemented in the first place. The UAE has over the years made it its mission to curd illegal activities emanating from its borders. Hence the idea to setup stringent rules designed to prevent financial crimes like money laundering and terrorism financing. It began with Federal Decree-Law No. 20 of 2018. In October 2025, a stronger law replaced it (Federal Decree-Law No. 10), introducing tougher penalties.

Not adhering to the laws could result in fines of up to AED 100 million. In worst case scenario, individuals can face prison terms up to 10 years. It also authorises authorities to investigate previous breaches without any time limits.

Who must comply with UAE’s anti money laundering laws?

The UAE Anti-Money Laundering Law applies essentially to two groups: Financial Institutions consisting of banks, insurance companies, and exchange houses, and Designated Non-Financial Businesses and Professions. Most business owners reading this fall into the DNFBP category.

DNFBPs include:

Real estate agents and property developers

Gold, diamond, and precious metals dealers

Accountants and auditors

Lawyers and legal consultants

Corporate service providers (company formation agents)

Virtual Asset Service Providers (cryptocurrency businesses)

During the first half of 2025, DNFBP violations broke down as follows:

Sector

Number of Violations

Fines Imposed

Precious Metals & Gemstones

473

AED 20 million

Real Estate

495

AED 18.5 million

Corporate Services & Auditors

95

AED 4 million

Total

1,063

AED 42+ million

These numbers represent just the first six months of 2025; total fines for the eight months exceeded AED 380 million when including banking sector penalties.

What are anti money laundering regulations in daily practice?

Understanding what anti money laundering regulations are means grasping how these laws affect your actual business operations. Three core requirements define compliance.

Customer Due Diligence (CDD)

Customer Due Diligence forms the foundation of anti-money laundering regulations. Before accepting any client, you must complete four steps:

1. Identity Verification

Verify each customer’s identity by reviewing original passports, Emirates IDs, or trade licences rather than relying on photocopies.

2. Beneficial Ownership Identification

Identify individuals who ultimately own or control 25% or more of any legal entity. The 2025 law made providing false beneficial ownership information a criminal offence, carrying severe penalties.

3. Understanding Business Purpose

Document why customers need your services, their business activities, expected transaction volumes, and source of funds. This creates a baseline for monitoring unusual activity.

4. Ongoing Monitoring

CDD isn’t a one-time task. Continuously monitor customer transactions, update information regularly, and investigate activities that don’t match customer profiles.

Risk-Based Customer Categories

Not every customer presents the same risk. Anti money laundering regulations require categorising clients:

Low Risk: Government entities and publicly listed companies receive Simplified Due Diligence.

Standard Risk: Most typical customers receive Standard Due Diligence.

High Risk: Politically Exposed Persons (PEPs), customers from high-risk countries, and cash-intensive businesses require Enhanced Due Diligence with senior management approval.

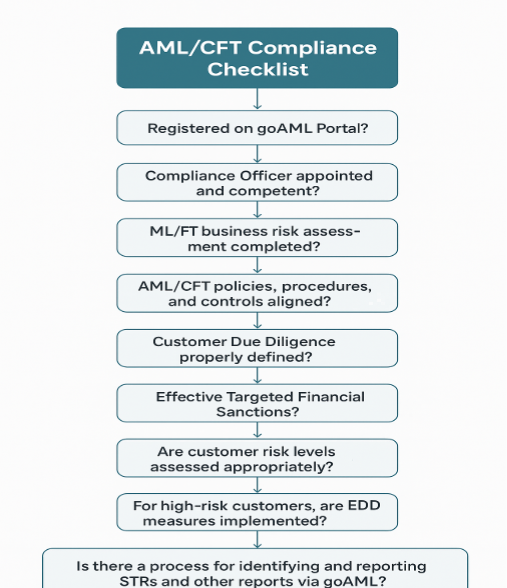

The goAML Platform

All DNFBPs must register on goAML, the UAE’s official platform for submitting Suspicious Transaction Reports (STRs) and Suspicious Activity Reports (SARs) to the Financial Intelligence Unit.

Registration requires your trade licence, a compliance officer designation letter, an officer’s passport and Emirates ID, and the installation of the Google Authenticator app. Failure to register attracts fines from AED 50,000 to AED 1 million. In 2025, authorities made goAML registration a primary inspection criterion.

Record Retention: Keep all customer due diligence records, transaction documentation, and compliance materials for five years minimum after ending business relationships. Records must be organised, searchable, and immediately available during regulatory inspections.

Why anti money laundering is important for your business?

Besides preventing fines, an understanding of why anti-money laundering is important shows strategic benefits leveraged for growth by sophisticated businesses.

Safeguarding UAE’s International Reputation

That changed in February 2024 when the UAE was removed from the FATF grey list. Such a development brought evidence of the nation’s compliance with international standards and boosted further confidence from abroad in businesses within the UAE.

When you comply with AML requirements, you help build this reputation. Robust national standards keep international banks willing to process UAE transactions, attract foreign investment, and maintain the UAE’s status as a trusted financial centre.

Avoiding Devastating Penalties

The financial consequences of non-compliance have increased dramatically: beyond the AED 380 million imposed across all sectors in eight months, there are sobering stories from individual penalties:

One exchange house received a record AED 200 million fine in May 2025.

Two foreign bank branches together paid AED 18.75 million (USD 5 million).

A Dubai International Financial Centre trader faced USD 25,000 (AED 91,813) in provisional fines.

An Abu Dhabi Global Market brokerage settled for USD 504,000 (AED 1.85 million).

Businesses in the past have seen licences suspended, operations restricted, and reputations damaged, often more costly than the monetary fines themselves. Several precious metals dealers had licences permanently revoked in 2025.

Maintaining Banking Relationships

Perhaps the most immediate reason why anti money laundering is important concerns banking access. UAE and international banks conduct rigorous checks on business customers, refusing accounts or transactions for entities with weak controls.

If you cannot demonstrate robust compliance programmes, documented policies, trained staff, proper records, banks will decline your business. This isn’t theoretical. Numerous SMEs discover this reality when attempting to open corporate accounts or establish payment facilities.

Strong anti-money laundering practices facilitate smooth banking relationships, faster transaction processing, and access to trade finance that fuels growth.

Building Client Trust

International clients, especially those from Europe, North America, and developed Asian markets, frequently demand proof of strong and active anti-money laundering programs before entering into any kind of partnership with UAE companies. Showing full compliance through various means such as certifications, written policies, and open practices will not only set your company apart from those who view the requirements as mere red tape but will also be of great help when vying for contracts with big players like multinationals, government agencies, or institutions that carry out their own due diligence.

Protecting Against Criminal Exploitation

Accordingly, criminals focus special attention on businesses with poor controls as vehicles for laundering proceeds. When your business unwittingly serves to facilitate money laundering, you risk not only regulatory fines but possible criminal prosecution.

The corporate criminal liability introduced by the 2025 law brought into prosecution companies themselves, not just individual perpetrators. Directors and managers could face up to 10 years’ imprisonment if they knew, or ought to have known, of illicit activities.

Robust controls create mechanisms for the detection of suspicious activities before they create any legal exposure, an invaluable defensive layer in high-risk sectors.

Core Compliance Requirements

Translating UAE anti money laundering law into practice requires implementing specific measures.

Appoint a Compliance Officer

Every business subject to anti money laundering regulations must designate a qualified Compliance Officer responsible for:

Overseeing AML programme implementation

Serving as a regulatory contact point

Submitting suspicious transaction reports through goAML

Conducting internal risk assessments

Coordinating staff training

Maintaining compliance documentation

This cannot be nominal. The Compliance Officer must have adequate power, material and direct access to senior management to carry out compliance duties effectively.

These policies must reflect your specific business. A gold dealer’s procedures differ substantially from an accounting firm. Generic, copied policies fail regulatory scrutiny.

Provide training during onboarding and refresh it at least annually. Document all sessions, maintain attendance records, and test comprehension.

Monitor Transactions

For businesses processing transactions, particularly cash or cross-border payments—systematic monitoring is essential:

Establish baseline expectations for each customer category

Flag transactions deviating from established patterns

Create investigation protocols for flagged transactions

Determine when suspicious activity reporting is warranted

Technology significantly enhances monitoring capabilities. Automated systems provide systematic surveillance that manual oversight cannot match.

Submit Suspicious Transaction Reports

When monitoring identifies potentially suspicious activities, UAE anti money laundering law mandates prompt reporting through goAML. Don’t wait for absolute proof, suspicion triggers reporting obligations.

Suspicious activities include:

Transactions with no apparent economic purpose

Customer reluctance to provide standard information

Unnecessarily complex structures for straightforward activities

Frequent deposits just below reporting thresholds

Transactions involving high-risk countries

Behaviour inconsistent with stated business

Note: Never inform customers that suspicious transaction reports have been filed. “Tipping off” constitutes a separate offence, potentially undermining investigations and generating additional penalties.

Industry-Specific Considerations for Anti money laundering law

Different sectors face unique risks and requirements.

1. Real Estate Professionals: With 495 violations and AED 18.5 million in fines during H1 2025, real estate faces intense scrutiny. Requirements include:

Reporting cash transactions at or above AED 55,000

Enhanced due diligence for virtual asset property purchases

Verifying source of funds for high-value transactions

Monitoring purchases from high-risk jurisdictions

Documenting property purchase purposes

2. Precious Metals Dealers: Leading violations (473 offences, AED 20 million in fines), this sector faces the toughest enforcement following 2024 licence suspensions. Requirements include:

Mandatory reporting of transactions at or above AED 55,000

Rigorous supplier and customer verification

Due diligence on metals and stones source

Enhanced international transaction screening

Detailed transaction documentation

3. Accountants and Auditors: Apply enhanced due diligence when:

Preparing or executing client transactions

Creating or managing legal entities

Managing client money or assets

Providing tax consultancy

Be vigilant when client structures appear unnecessarily complex or beneficial ownership remains unclear.

4. Corporate Service Providers: Companies providing business formation or registered office services must:

Understand commercial rationale for structures created

Monitor ongoing activities of entities you serve

Report suspicions about structures used for illicit purposes

Refuse establishing structures when beneficial ownership can’t be verified

Conclusion

The anti-money laundering landscape in the UAE has evolved to a regime of strict, FATF-aligned laws under Federal Decree Law No. 10 of 2025, replacing prior laws with tougher penalties up to AED 100 million, expanded corporate liability, and stronger enforcement powers, including the extended freezing of funds.

The evolution will challenge the minimal-compliance competitors through fines, AED 380 million in eight months, the revocation of licenses, and prosecutions, whereas proactive businesses build trust with banks, clients, and regulators for a competitive advantage.

Act now: register on goAML; designate a compliance officer and carry out risk assessments-requirements necessary in real estate, precious metals, services, or corporate formation to avoid non-compliance that is much costlier.